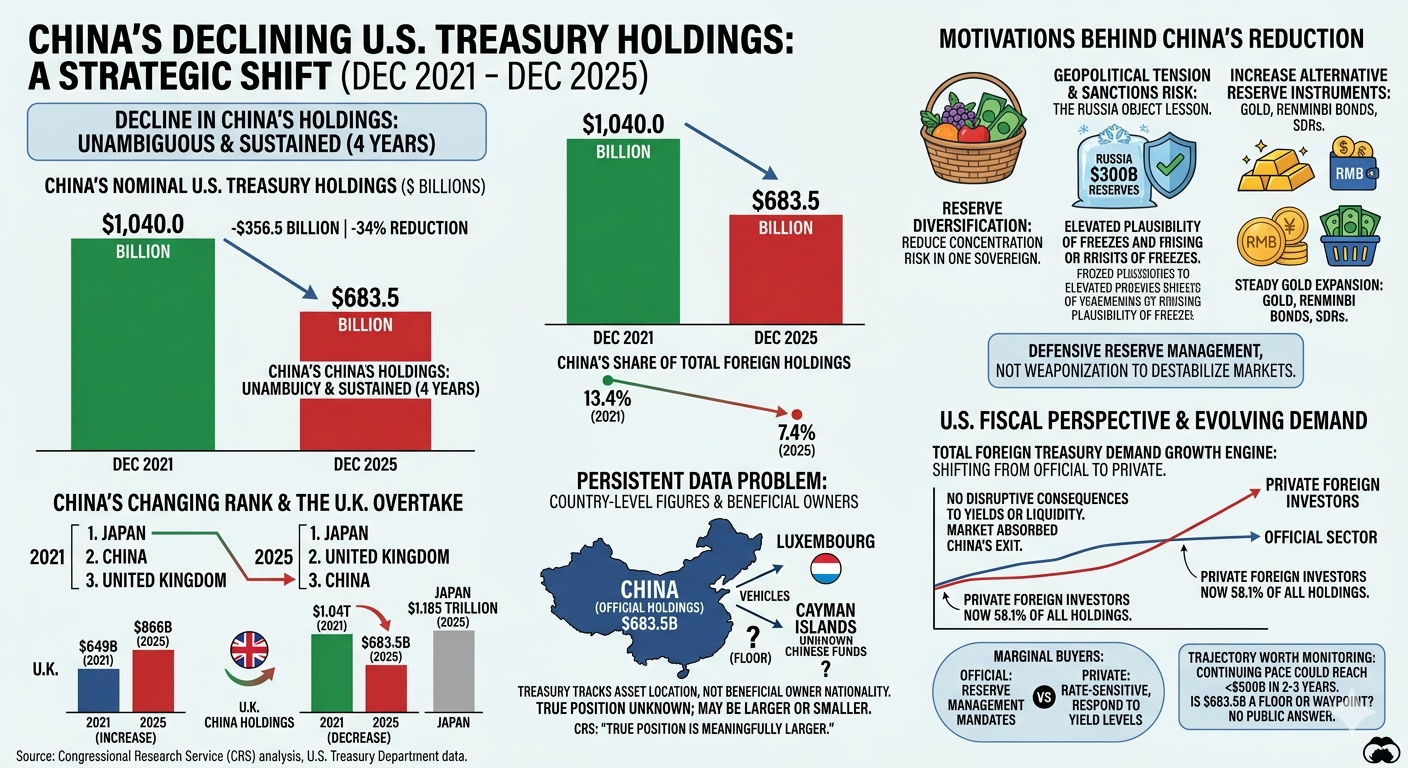

China Has Shed $357 Billion in U.S. Treasuries Since 2021

China held $1.04 trillion in U.S. Treasury securities as of December 2021. By December 2025, that position had declined to $683.5 billion — a reduction of roughly $357 billion, or 34%, over four years. China remains the third-largest foreign holder of U.S. federal debt, but its share of total foreign holdings fell from 13.4% to 7.4% over the same period. The trajectory is unambiguous and sustained.

The decline has been both nominal and relative. In 2021 China ranked second among foreign holders, behind only Japan. It now sits in third place, overtaken by the United Kingdom whose holdings expanded from $649 billion to $866 billion during the same interval. The rank-order shift is a reasonable proxy for the broader repositioning underway in China’s reserve management strategy, though interpreting it with precision requires acknowledging a persistent data problem.

Treasury’s country-level figures track asset location, not beneficial owner nationality. A Chinese sovereign entity investing through a Luxembourg or Cayman Islands vehicle appears in those jurisdictions’ totals rather than in China’s. The $683.5 billion figure is therefore a floor, not a ceiling, on Chinese exposure to U.S. federal debt. CRS has noted this explicitly in its analysis. The true position is unknown and may be meaningfully larger. Conversely, it may have declined even more sharply on a beneficial-ownership basis than the headline figure suggests.

The motivations behind China’s reduction are multiple and not mutually exclusive. Reserve diversification is the most straightforward: holding a third of reserves in a single foreign sovereign’s paper carries concentration risk that becomes more salient as geopolitical tension elevates the plausibility of sanctions or asset freezes. Russia’s experience following the 2022 invasion of Ukraine — with roughly $300 billion in central bank reserves immobilized by Western governments — provided an object lesson that China’s monetary authorities have been publicly processing. Reduced Treasury accumulation could reflect a deliberate effort to lower vulnerability to that scenario.

Dollar-denominated assets also lose relative appeal when the bilateral relationship deteriorates and when alternative reserve instruments — gold, renminbi-denominated bonds, SDR allocations — become incrementally more viable. China’s gold reserves have expanded steadily since 2022. Neither development requires assuming a coordinated policy of weaponizing Treasury holdings; the reduction is more easily explained by defensive reserve management than by any intention to destabilize U.S. debt markets.

From a U.S. fiscal perspective, the reduction has not produced the disruptive consequences that some analysts anticipated. Treasury markets absorbed China’s gradual exit without measurable disruption to yields or liquidity. Other foreign private investors, particularly those in the United Kingdom and elsewhere, expanded their positions as China’s declined. The structural demand for Treasuries as reserve collateral and as dollar-liquidity instruments has proven more durable than any single country’s allocation choices. Japan, still the largest foreign holder at $1.185 trillion, has also trimmed from its 2021 peak of $1.3 trillion, but has remained broadly stable.

What China’s declining position does signal is that the era of rapidly accumulating foreign official holdings — which peaked globally in 2020 — has ended. The official sector is no longer the growth engine of Treasury demand. Private foreign investors now account for 58.1% of all foreign holdings, and it is their behavior, not Beijing’s, that will increasingly determine how external demand for U.S. debt evolves. That shift changes the dynamics: private investors are more rate-sensitive and less bound by reserve management mandates, which makes the marginal foreign buyer of Treasuries more likely to respond to yield levels than to geopolitical calculations.

The trajectory of China’s holdings is worth monitoring. A continuation of the current pace would bring the position below $500 billion within two to three years. Whether that level represents a floor — defined by genuine reserve needs and financial system integration — or a waypoint toward further reduction is a question Beijing’s monetary authorities are unlikely to answer publicly.